India’s non-fossil capacity crosses 53% of installed base

India’s total installed power capacity stood at 542,354 MW as of May 31, 2026, according to data released by the Central Electricity Authority (CEA). Non-fossil fuel sources accounted for 53.75% of the total installed capacity, while fossil fuel sources represented 46.25%.

The figures indicate a structural shift in India’s generation mix, although coal continues to dominate actual electricity generation. Installed capacity reflects the available generation base, while electricity generation depends on utilisation levels across technologies.

Solar capacity rises

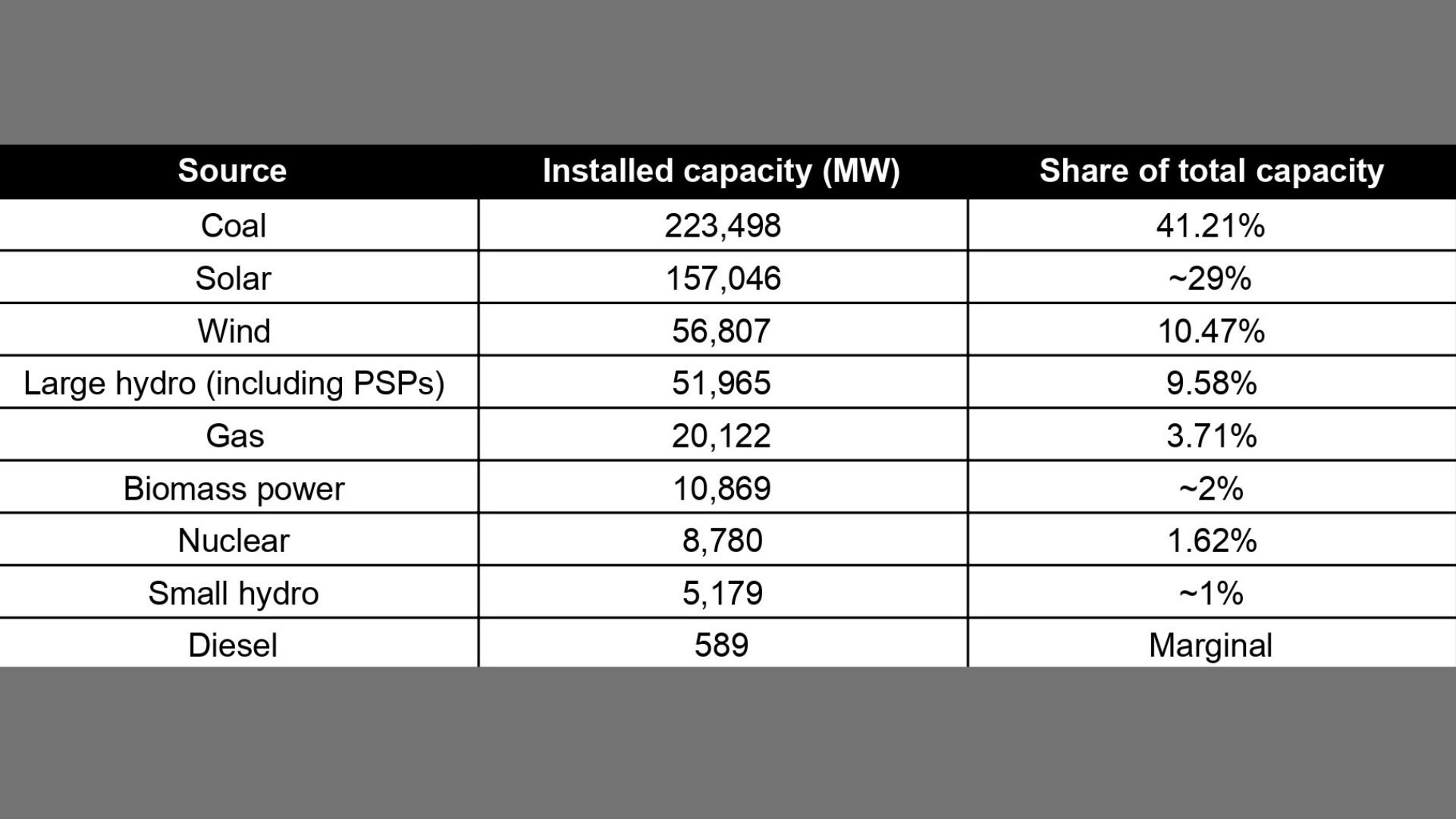

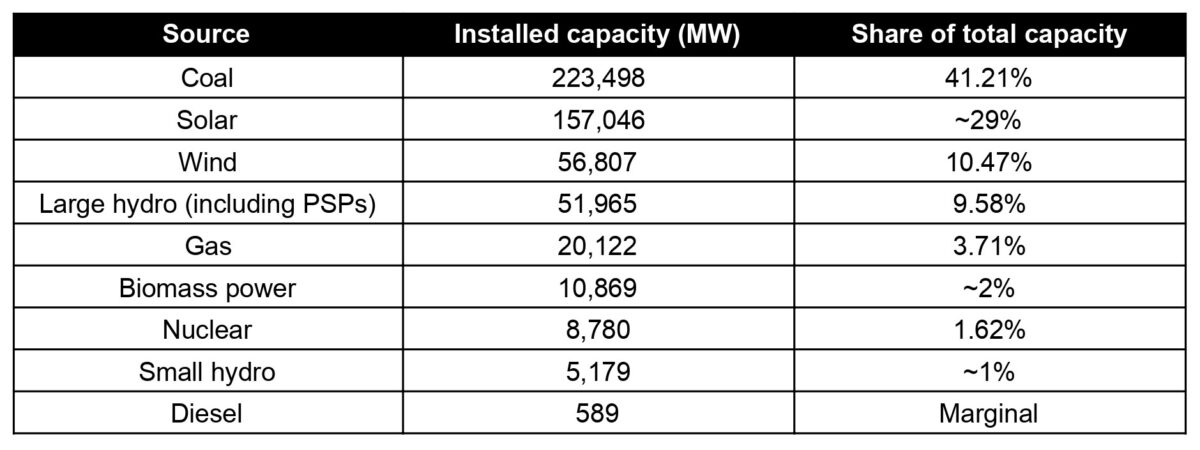

Solar power capacity reached 157,046 MW, making it India’s second largest installed source after coal at 223,498 MW. Solar now accounts for nearly 29% of total installed capacity, compared to a single-digit share earlier in the decade.

Wind capacity stood at 56,807 MW, or 10.47% of the total. Combined wind and solar capacity reached 213,853 MW, representing around 39% of India’s installed base. Including large hydro at 51,965 MW, biomass power at 10,869 MW, and small hydro at 5,179 MW, total renewable capacity stood at 282,745 MW.

Private sector developers accounted for the majority of the 230,780 MW in renewable energy capacity under the Ministry of New and Renewable Energy (MNRE). In the Northern Region, private developers held 56,591 MW of renewable capacity, compared to 6,026 MW under the central sector.

Coal remains dominant

Coal remained India’s largest individual power source at 223,498 MW, accounting for 41.21% of total installed capacity.

Two coal-based units were commissioned in May 2026. Patratu Thermal Power Station (TPS) Unit 2 of PVUNL with a capacity of 800 MW was commissioned in Jharkhand on May 11, 2026, while Yadadri TPS Unit 3 of TGGENCO with a capacity of 800 MW was commissioned in Telangana on May 13, 2026.

According to CEA data, coal capacity of 1,995 MW, gas capacity of 4,225.84 MW, and nuclear capacity of 100 MW have remained excluded from the installed base since May 31, 2025, due to extended outages. If these units return to service, India’s total installed capacity would exceed 548 GW.

Gas-based capacity stood at 20,122 MW, accounting for 3.71% of the total, with no new additions recorded in May. Diesel-based capacity remained limited at 589 MW, largely concentrated in island territories and the North-East.

Hydro and nuclear additions

Nuclear capacity stood at 8,780 MW, or 1.62% of the installed base, across central sector stations.

Hydro capacity, including pumped storage plants (PSPs), reached 51,965 MW. During FY 2026-27, THDC commissioned Tehri PSP Unit 4 with a capacity of 250 MW in April, while NHPC commissioned Subansiri Lower Unit 4 with a capacity of 250 MW in May. JSW also commissioned Tidong-I Unit 1 with a capacity of 50 MW in May.

Total capacity additions during FY 2026-27 so far stood at 3,189.79 MW in renewable sources and 1,900 MW in conventional sources, resulting in net additions of 5,089.79 MW.

Regional distribution

The Western Region had the largest installed base at 186,681 MW. Maharashtra accounted for 62,199 MW, Gujarat for 74,219 MW, and Madhya Pradesh for 29,774 MW. Gujarat’s solar additions contributed significantly to its installed capacity growth.

The Southern Region accounted for 151,276 MW and remained the largest renewable energy hub. Tamil Nadu had 47,960 MW of installed capacity, Karnataka 38,550 MW, Andhra Pradesh 30,726 MW, Telangana 22,689 MW, and Kerala 8,191 MW.

The Northern Region accounted for 157,402 MW, led by Uttar Pradesh at 37,241 MW and Rajasthan at 65,560 MW. Rajasthan’s solar additions placed it among the top five states by installed capacity.

The Eastern Region had 40,483 MW of installed capacity, while the North-Eastern Region accounted for 6,347 MW. The Islands accounted for 164 MW, primarily based on diesel and small-scale solar systems.

Capacity and generation gap

The rise in non-fossil installed capacity does not mean that more than half of India’s electricity generation comes from clean sources. Installed capacity measures available infrastructure, while actual generation depends on plant load factor and operating patterns.

Coal-based plants generally operate at higher load factors than solar and wind projects, which depend on weather conditions. As a result, India’s electricity generation mix continues to remain heavily dependent on coal despite the increase in renewable capacity.

The growth in renewable capacity is also driving demand across the transmission and transformer equipment segment. The expansion of renewable generation capacity has increased the requirements for step-up transformers, grid substations, and transmission corridors connecting renewable-rich states with demand centres.