China’s solar firms are bleeding and winning at once

Author: PPD Team Date: March 24, 2026

Author: PPD Team Date: March 24, 2026

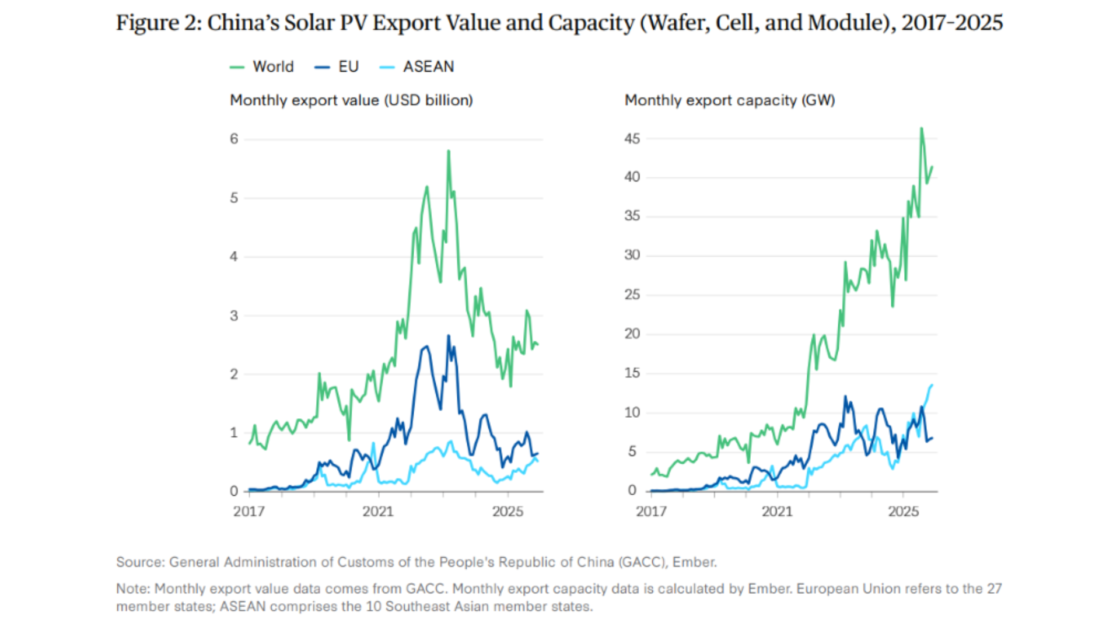

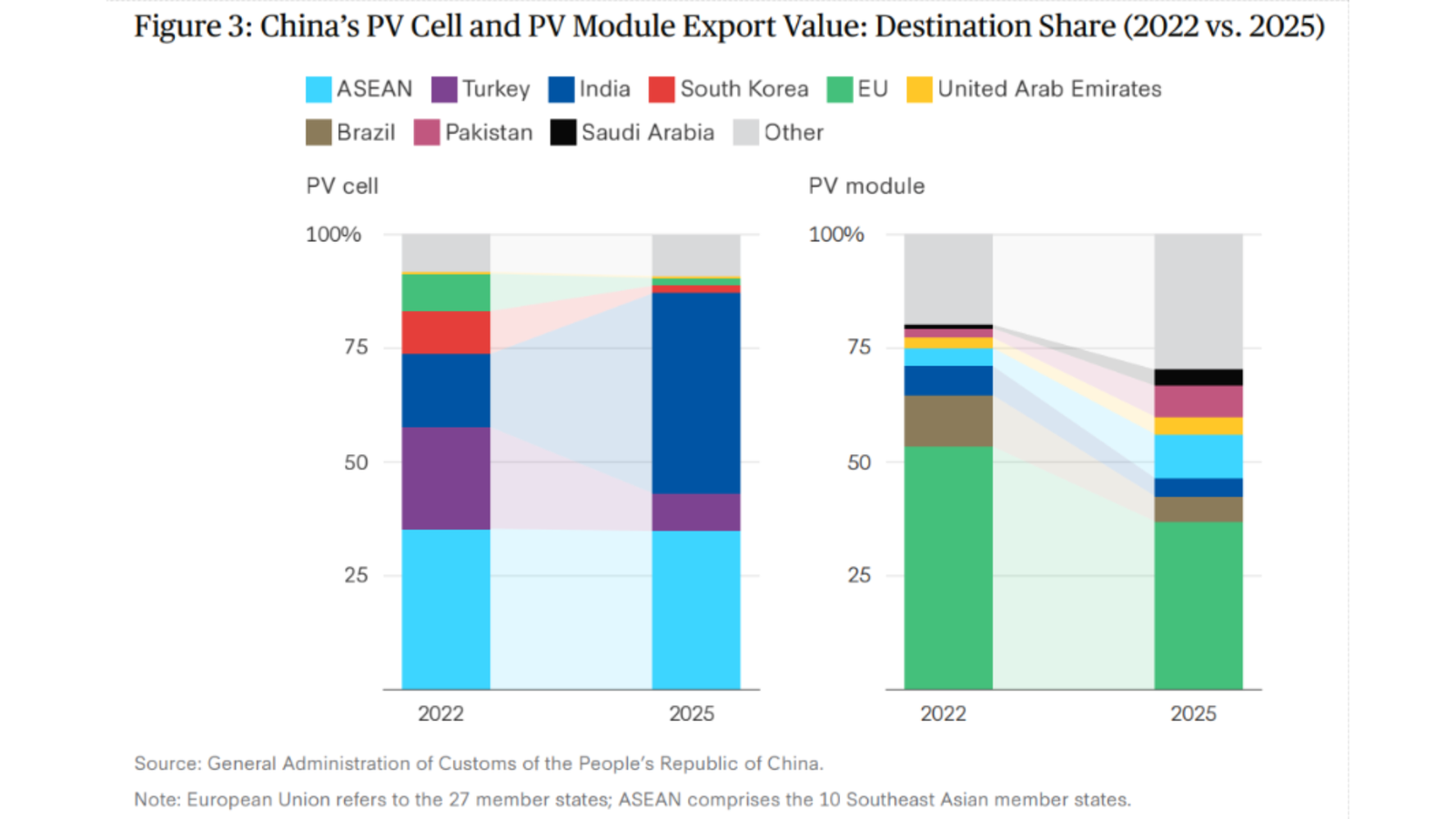

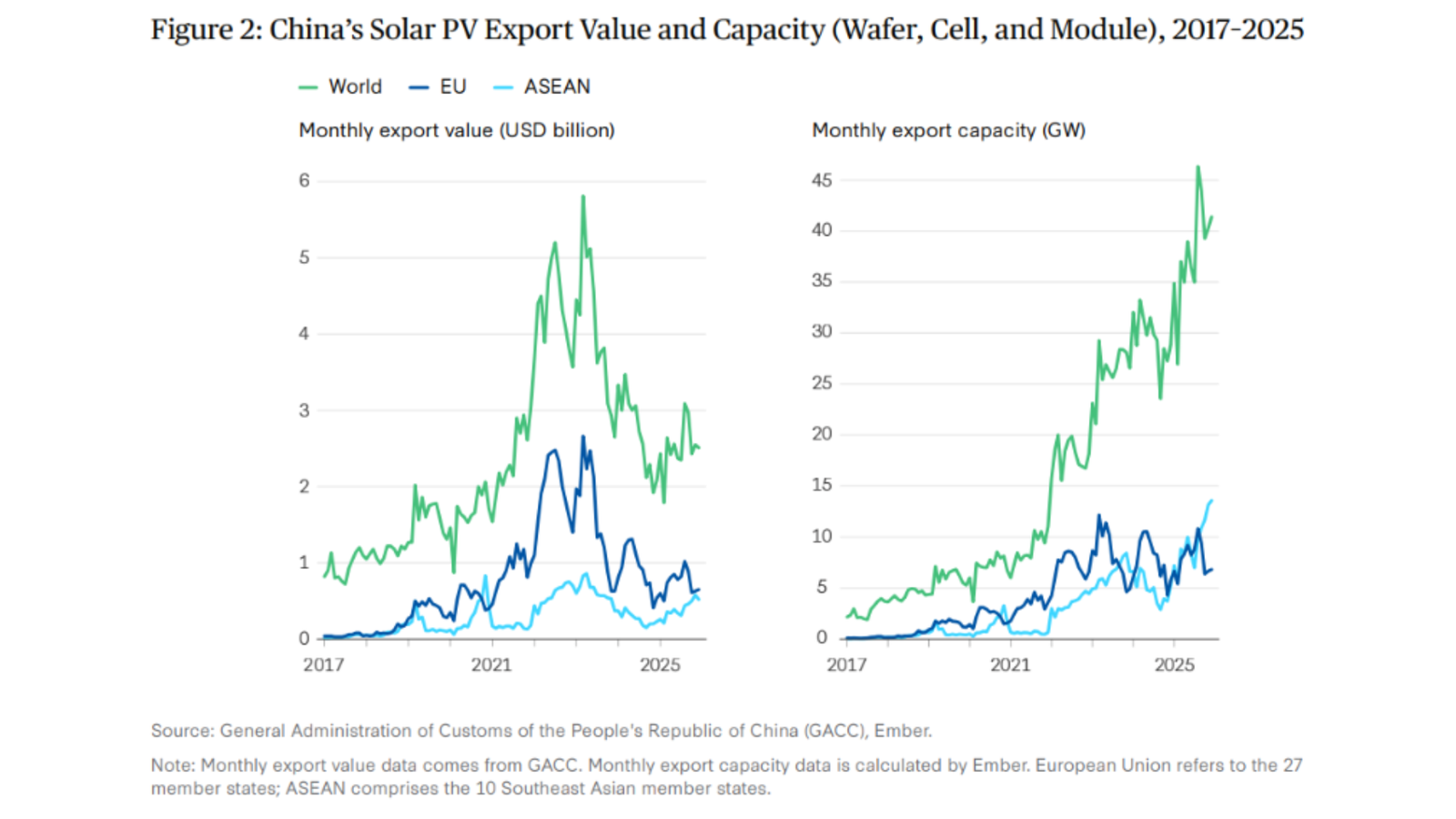

China’s solar industry is undergoing its sharpest downturn in over a decade, with global implications for prices, supply chains, and competition. A March 2026 brief by the Center for Strategic and International Studies (CSIS) states that price erosion, excess capacity, and rising trade barriers are disrupting the sector while reinforcing China’s structural dominance.

The CSIS brief, authored by Michael Davidson and Sandy Qian, identifies oversupply as the central issue. In 2024, global photovoltaic (PV) manufacturing capacity exceeded installation demand by more than two times, according to the International Energy Agency (IEA). Module prices declined by 50% in 2023 and a further 25% in 2024, while polysilicon prices fell over 70% in 2023 and another 40% in 2024.

The downturn has triggered consolidation. China’s five largest solar firms, Jinko Solar, Trina Solar, JA Solar, LONGi Green Energy, and Tongwei, reduced their combined workforce by over 30% last year. More than 40 smaller firms have exited, been acquired, or shut operations. In December 2025, Chinese regulators introduced a fund aimed at retiring nearly one-third of low-efficiency polysilicon capacity.

China retains supply chain lead

Despite industry stress, China’s dominance across the PV value chain remains intact. In 2024, it accounted for 93.2% of global polysilicon production, 96.6% of wafers, 92.3% of PV cells, and 86.4% of modules, as per China Photovoltaic Industry Association data.

China has also strengthened its position in solar technology. Its share of global solar patent filings reached about 65% in 2024, up from 13% in 2004. The sector has rapidly adopted tunnel oxide passivated contact (TOPCon) technology. LONGi Green Energy holds the global efficiency record for perovskite/silicon tandem cells at 34.85%, according to the National Renewable Energy Laboratory’s January 2026 chart.

Pressure on non-Chinese manufacturers

Falling prices are placing significant strain on manufacturers outside China. European and United States (U.S.) producers, with cost structures 50% to 100% higher than Chinese imports, are facing closures despite policy support. Norwegian Crystals ceased operations in 2023. Meyer Burger shut its Germany facility in 2024 and its U.S. plant in 2025.

Policy direction and outlook

The CSIS brief states that competing with China on current-generation cost structures is not feasible in the near term. It recommends focusing industrial policy on next-generation solar technologies, particularly beyond-tandem innovations where supply chains are still emerging. It also cautions that broad non-China sourcing mandates may weaken domestic industry competitiveness.

The brief concludes that the ongoing consolidation is not creating space for new global leaders. Instead, it is resulting in a more efficient and technologically advanced Chinese solar industry with deeper integration into global supply chains.

Source for images: Center for Strategic and International Studies (CSIS), based on GACC and Ember.

Author: PPD Team Date: November 4, 2024 AM Green has placed an order with John Cockerill for a 1.3 GW advanced pressurised alkaline electrolyser for its existing plant in Kakinada, Andhra Pradesh. This marks the largest electrolyser order in India to date. The project, set to begin production in the second half of 2026, will supply electrolysers in two phases of 640 MW each. It aims to produce green hydrogen and convert it into green…

Author: PPD Team Date: January 23, 2025 NTPC Renewable Energy Limited (NTPC REL), a subsidiary of NTPC Limited through NTPC Green Energy Limited, has commenced commercial operation of the second part capacity of its 200 MW Sadla Solar PV Project in Gujarat. The additional 25 MW capacity became operational on January 17, 2025. Earlier, the first part capacity of 37.5 MW was commissioned on December 21, 2024.

Author: PPD Team Date: January 6, 2026 Rajesh Power Services Limited has received a Letter of Intent (LoI) from Gujarat Urja Vikas Nigam Limited (GUVNL) for developing a 65 MW / 130 MWh standalone Battery Energy Storage System (BESS) facility at Virpore in Gujarat. The company informed the stock exchanges about the award on January 5, 2026. The project forms part of Phase VII of a tariff-based competitive bidding process and will receive Viability Gap…

Author: PPD Team Date: December 26, 2024 REC Power Distribution Company Limited (REC PDCL) incorporated Rajgarh III Power Transmission Limited, a special purpose vehicle (SPV) for the development of the Transmission system for Evacuation of Power from RE Projects in Rajgarh (1500 MW) SEZ in Madhya Pradesh-Phase III on December 24, 2024. REC PDCL has been appointed as the bid process coordinator (BPC) for the selection of a transmission service provider (TSP) for the establishment…

Author: PPD Team Date: April 9, 2025 Kundan Green Energy has taken over an 11.5 MW operational waste-to-energy plant in Jabalpur, Madhya Pradesh. The acquisition was made through insolvency proceedings under the Insolvency and Bankruptcy Code, 2016. The process was initiated by the State Bank of India and completed via the National Company Law Tribunal. The acquired facility, previously operated by the Essel Group under Jabalpur MSW Private Limited, processes about 450 tonnes of municipal…

Author: PPD Team Date: April 3, 2025 Dineshchandra R Agrawal Infracon Private Limited (DRAIPL), Sterling and Wilson, and Advait Energy Transitions Limited have secured engineering, procurement, and construction (EPC) contracts for major solar projects in Gujarat and Rajasthan. DRAIPL secures 200 MW Khavda solar EPC contract DRAIPL has won an EPC contract from NHPC Limited for the 200 MW Khavda Solar PV Project – Phase XXIII. The project is part of Gujarat State Electricity Corporation…