India’s power challenge moves beyond generation to system optimisation

Author: PPD Team Date: January 19, 2026

India’s power sector has transitioned from addressing chronic shortages to managing a complex landscape of over-capacity, urban distribution challenges, and a large industrial self-generation fleet, according to official data. Recent reports from the Central Electricity Authority (CEA) indicate the national priority is shifting from simply adding generation capacity to optimising utilisation and integrating diverse energy sources.

The Central Electricity Authority (CEA), in its reports All India Electricity Statistics – General Review and Growth of Electricity Sector in India from 1947-2025, details this evolution. The data show that energy and peak deficits have effectively been eliminated, falling to approximately 0.1% and 0%, respectively. The current challenge lies in operational reliability, urban distribution bottlenecks, and navigating a dual-system structure.

While renewable energy sources (RES) now constitute over one-third of India’s installed capacity, they contributed only about 14% of total utility generation in the period reviewed. Coal and lignite provided approximately 73%, highlighting a significant capacity-utilisation gap. This establishes a “dual system” where coal primarily meets baseload energy demand, while RES helps meet peak demand and regulatory compliance.

A major focal point is the scale of captive power generation, which functions as a parallel grid. Behind-the-meter plants, with roughly 82 GW of capacity generating over 235 TWh, are predominantly coal-based, accounting for about 80% of their output. The iron and steel sector alone generates over 60 TWh from its own plants. This substantial industrial self-generation fleet presents a critical frontier for national decarbonization efforts.

The pattern of electricity consumption is also evolving. Although the industrial sector remains the largest single consumer at 41.6%, the combined share of domestic and agricultural consumption now exceeds 41%. The fastest annual growth in 2023-24 was recorded in commercial, traction (railways), and agricultural segments, indicating load growth is increasingly driven by electrified transport, urban services, and irrigation.

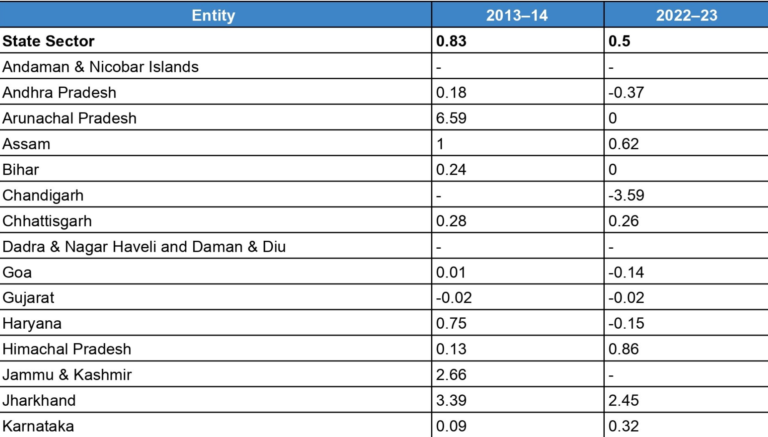

Significant progress has been made in reducing technical and commercial losses during transmission and distribution (T&D), which have fallen from over 30% in the mid-2000s to approximately 17–18% in 2023-24. However, further improvements will require targeted, state-specific interventions rather than broad, low-effort solutions. India’s per-capita electricity consumption, at about 1,400 kWh, remains well below that of China (~6,100 kWh) and OECD nations.

Regional disparities persist, with North-Eastern and some northern regions still experiencing T&D losses of 20% or higher. Future national gains will depend on targeted governance and consumer engagement in these areas. Additionally, underdeveloped hydro potential in eastern and northeastern basins presents an opportunity for storage-like hydro and pumped storage projects to provide grid flexibility, though these come with socio-environmental complexities.

The insights point to a sector where the next phase of development hinges on improving utilisation, modernising urban delivery networks, and transitioning the captive power base.

The featured photograph is for representation only.